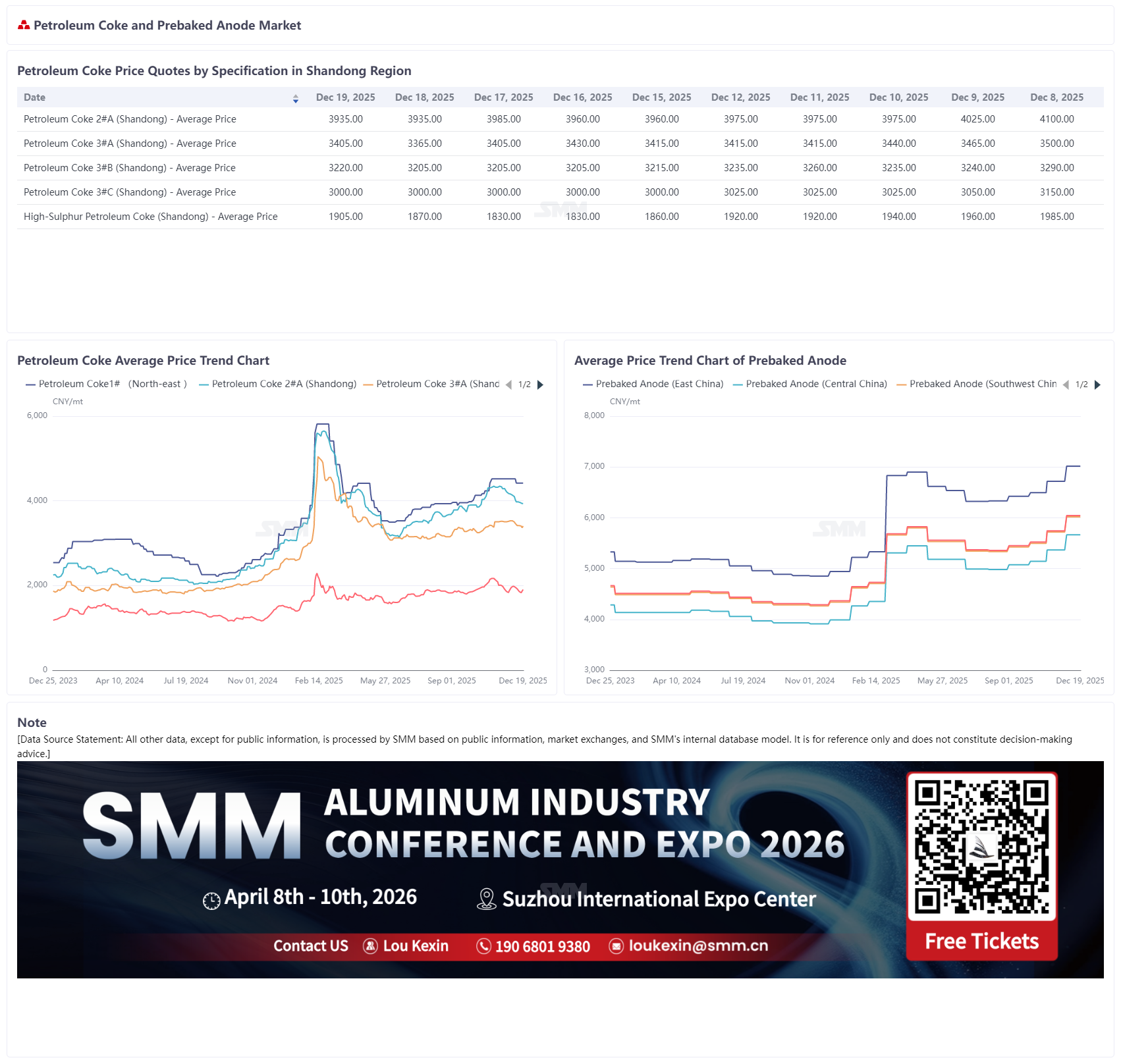

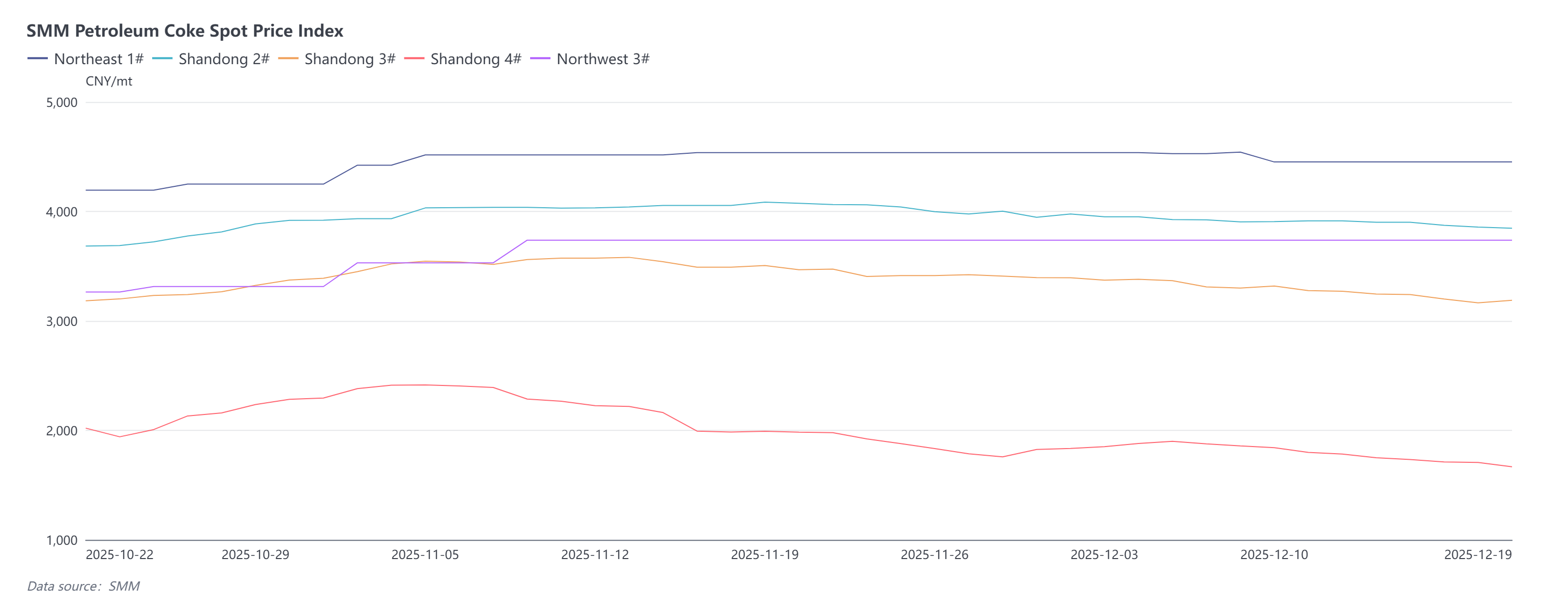

Recently, the petroleum coke market continued to see weak trading sentiment, with refinery petroleum coke prices largely stable to lower. Specifically, PetroChina's refinery petroleum coke prices were mixed this week, with adjustments ranging from 50-150 yuan/mt; current prices are concentrated at 4,150-4,200 yuan/mt. Among them, Taizhou Petrochemical's petroleum coke indicators improved, and its petroleum coke price was raised by 150 yuan/mt mid-week. PetroChina's low-sulphur petroleum coke prices in north-east China remained stable, with current petroleum coke prices concentrated at 4,096-4,706 yuan/mt. SMM's spot price index for #1 petroleum coke in north-east China was 4,451.9 yuan/mt. Mid-sulphur petroleum coke prices in north-west China operated steadily, with SMM's spot price index for #3 petroleum coke in north-west China at 3,737.42 yuan/mt. Sinopec's refinery petroleum coke shipments were stable, and petroleum coke prices were largely steady; however, prices for some refineries' mid and high-sulphur petroleum coke were lowered, and due to slower procurement from downstream anode plants, some refineries' anode-grade coke saw slight drops within 100 yuan. Local refineries faced poor shipments, with petroleum coke prices continuing to weaken, especially #4 coke, which saw more pronounced declines. The latest SMM data show that the spot price index for #2 petroleum coke in Shandong was 3,846.42 yuan/mt, down 1.72% WoW; the spot price index for #3 petroleum coke in Shandong was 3,188.45 yuan/mt, down 2.53% WoW; and the spot price index for #4 petroleum coke in Shandong was 1,667.61 yuan/mt, down 6.54% WoW.

This week, the imported petroleum coke market continued to see sluggish trading sentiment, with low downstream purchase willingness and few new orders, keeping prices under downward pressure. By category, low-sulphur petroleum coke saw clear pullbacks in transaction prices as some suppliers actively increased shipments amid weak market trading; the mid and high-sulphur petroleum coke market also performed weakly, with overall sluggish shipments, and port spot prices fell further, influenced by the ongoing decline in domestic high-sulphur petroleum coke prices. The weak performance in the import market echoed changes in the domestic petroleum coke supply-demand pattern.

On the supply side, Keyuan Petrochemical's short-term maintenance ended mid-week, while other major domestic refineries maintained steady production pace, resulting in a supply profile characterized by localized increases and overall stability. Looking ahead, as the number of new maintenance events decreases and previously idled units gradually resume production, market supply scale is expected to continue expanding.

Demand side, overall weakness and structural divergence were observed. In the short term, downstream enterprises exhibited strong wait-and-see sentiment, with procurement behavior dominated by just-in-time needs and weakened initiative to restock, leading to sluggish market purchase atmosphere and significant downward pressure on petroleum coke prices. By segment, in the carbon used in aluminum production sector—a core downstream for petroleum coke—operating rates in traditional key production areas like Shandong, Henan, and Hebei were under pressure due to enhanced environmental protection-related controls; however, new prebaked anode projects in regions like Inner Mongolia and Yunnan commenced operations and gradually released capacity, effectively improving supply elasticity in the carbon used in aluminum production market. This not only compensated for periodic production gaps caused by environmental protection-driven production restrictions and equipment maintenance in some areas but also supported the scale of just-in-time procurement for petroleum coke. The negative electrode materials sector maintained stable operations, and its just-in-time procurement of petroleum coke also provided some market support.

Overall, although the rigid demand for carbon used in aluminum production and anode materials provides some support to the market, it is insufficient to offset the pressure from overall weak demand. Against the backdrop of continuously increasing supply, petroleum coke prices have entered a sustained downward trend. Based on the above supply-demand pattern, SMM expects petroleum coke prices to remain in the doldrums in the short term. However, the market holds expectations for a recovery in January 2026, with the core driver being the concentrated release of stockpiling demand from downstream enterprises ahead of the Chinese New Year holiday, which is expected to provide temporary support to the market.